PUBLISHED January 22, 2026

According to the Dai-ichi Life Research Institute’s “Japan Economic Outlook” report, Japan’s economy is expected to maintain modest growth through the end of 2025 and into 2026.

Fiscal year GDP for 2025 is projected at around +0.9%, slightly revised downward from earlier forecasts. Economic activity experienced a contraction in the July–September quarter, largely due to weak residential investment and exports. Despite this, broader forward-looking indicators remain stable enough to support cautious optimism. Supportive global conditions, including a stabilizing U.S. economy, are expected to benefit Japan in 2026. Real wage stabilization is also anticipated to contribute to domestic demand. Overall, growth remains moderate and uneven across sectors.

Consumer demand shows tentative signs of strengthening, especially where wages are stabilizing. Spring 2026 wage negotiations are projected to yield continued pay increases, boosting household income. Real wages are expected to bottom out after persistent inflation pressures ease in 2025. With bolstered income growth, consumer spending may become a more reliable driver of growth next year. However, high living costs still weigh on purchasing power, limiting robust consumption expansion. Slower inflation is anticipated to reduce cost pressures gradually. As such, private demand is likely to remain a key underpinning of growth in 2026.

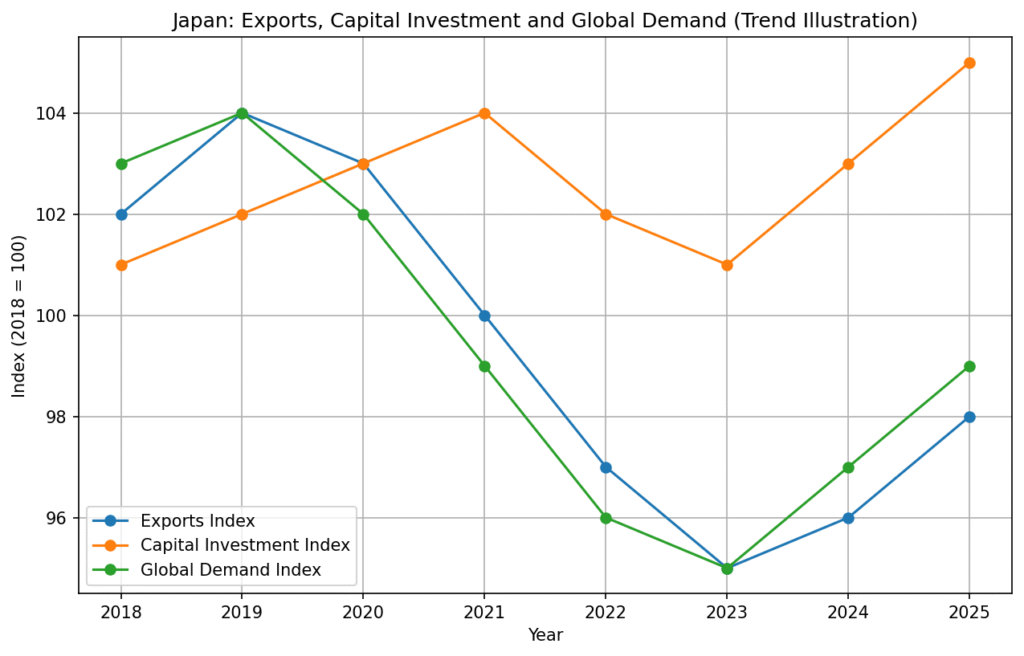

Export performance around mid-2025 was weak, reflecting global trade uncertainties and tariff impacts. Residential investment also fell sharply in the third quarter, dragging down quarterly GDP. Business investment is expected to pick up slowly as firms gain confidence in future demand. External demand remains soft, particularly in Asia and for goods exports. Global economic conditions, including U.S. and Chinese demand, remain significant risk factors. Despite this, international stabilization and interest rate cuts abroad could help Japan’s export recovery in 2026. Downward pressure on exports is likely to ease only gradually.

Consumer behaviour is central to Japan’s near-term outlook. As real wages stabilize, households are expected to maintain some level of spending growth. Structural pressures from inflation have weighed on consumer confidence, but easing price pressures offer relief. Labour market conditions, including wage negotiations and employment stability, are critical for sustaining spending. Private consumption may not surge dramatically, but it remains a consistent supporter of economic activity. Service sector demand, rather than manufacturing, is likely to be a key contributor going forward. Overall, demand from households underpins cautious optimism for 2026.

Japan’s export sector has remained under pressure throughout the second half of 2025, mainly due to weaker global demand and ongoing trade-related uncertainties. Shipments to key Asian markets have slowed, while higher tariffs and tighter financial conditions abroad have further limited growth opportunities for manufacturers. Business investment shows early but cautious signs of recovery. Large corporations continue to invest in digitalization, automation, and energy efficiency, while smaller firms remain more hesitant amid uncertain sales prospects. Capital spending is therefore improving unevenly across industries, with services and technology outperforming traditional manufacturing. Global risks continue to shape the outlook. Sluggish growth in China, geopolitical tensions, and fragile European demand all pose potential threats to Japan’s export-oriented economy. At the same time, expected monetary easing in major economies could gradually support international trade and improve financing conditions for Japanese companies. Looking ahead, exports are likely to recover only slowly, while domestic investment may become a more important growth driver. Together, these trends suggest that external conditions will remain a constraint in the short term, even as structural investment supports longer-term stability.

Japan’s economic trajectory as 2025 ends is one of measured progress amid persistent challenges. GDP growth projections near +0.9% reflect slow but stable momentum, anchored by wage support and domestic demand. However, weak external trade performance and sectoral contractions underscore the fragility of the recovery. As price pressures ease and global conditions stabilize, the Japanese economy is poised for modest improvement heading into 2026, even while risks from global policy shifts and soft overseas demand remain salient.

Consumer behaviour is central to Japan’s near-term outlook. As real wages stabilize, households are expected to maintain some level of spending growth. Structural pressures from inflation have weighed on consumer confidence, but easing price pressures offer relief. Labour market conditions, including wage negotiations and employment stability, are critical for sustaining spending. Private consumption may not surge dramatically, but it remains a consistent supporter of economic activity. Service sector demand, rather than manufacturing, is likely to be a key contributor going forward. Overall, demand from households underpins cautious optimism for 2026.

Japan’s export sector has remained under pressure throughout the second half of 2025, mainly due to weaker global demand and ongoing trade-related uncertainties. Shipments to key Asian markets have slowed, while higher tariffs and tighter financial conditions abroad have further limited growth opportunities for manufacturers. Business investment shows early but cautious signs of recovery. Large corporations continue to invest in digitalization, automation, and energy efficiency, while smaller firms remain more hesitant amid uncertain sales prospects. Capital spending is therefore improving unevenly across industries, with services and technology outperforming traditional manufacturing. Global risks continue to shape the outlook. Sluggish growth in China, geopolitical tensions, and fragile European demand all pose potential threats to Japan’s export-oriented economy. At the same time, expected monetary easing in major economies could gradually support international trade and improve financing conditions for Japanese companies. Looking ahead, exports are likely to recover only slowly, while domestic investment may become a more important growth driver. Together, these trends suggest that external conditions will remain a constraint in the short term, even as structural investment supports longer-term stability.

Japan’s economic trajectory as 2025 ends is one of measured progress amid persistent challenges. GDP growth projections near +0.9% reflect slow but stable momentum, anchored by wage support and domestic demand. However, weak external trade performance and sectoral contractions underscore the fragility of the recovery. As price pressures ease and global conditions stabilize, the Japanese economy is poised for modest improvement heading into 2026, even while risks from global policy shifts and soft overseas demand remain salient.