PUBLISHED February 28, 2026

According to the Daiwa Institute of Research’s “Japan’s Economy: Monthly Outlook (Jan 2026)”, Japan is heading into a prolonged period of modest but stable economic growth, supported by wages, exports and capital investment, while demographic decline and rising interest rates will increasingly weigh on the longer-term trajectory.

The report presents a revised medium-term baseline that underscores both the resilience and the structural constraints of the Japanese economy.

Growth Seen Averaging Below 1%

DIR projects that Japan’s real GDP will grow by an average of about 0.8% annually between FY2026 and FY2035, highlighting the country’s continued low-growth environment.

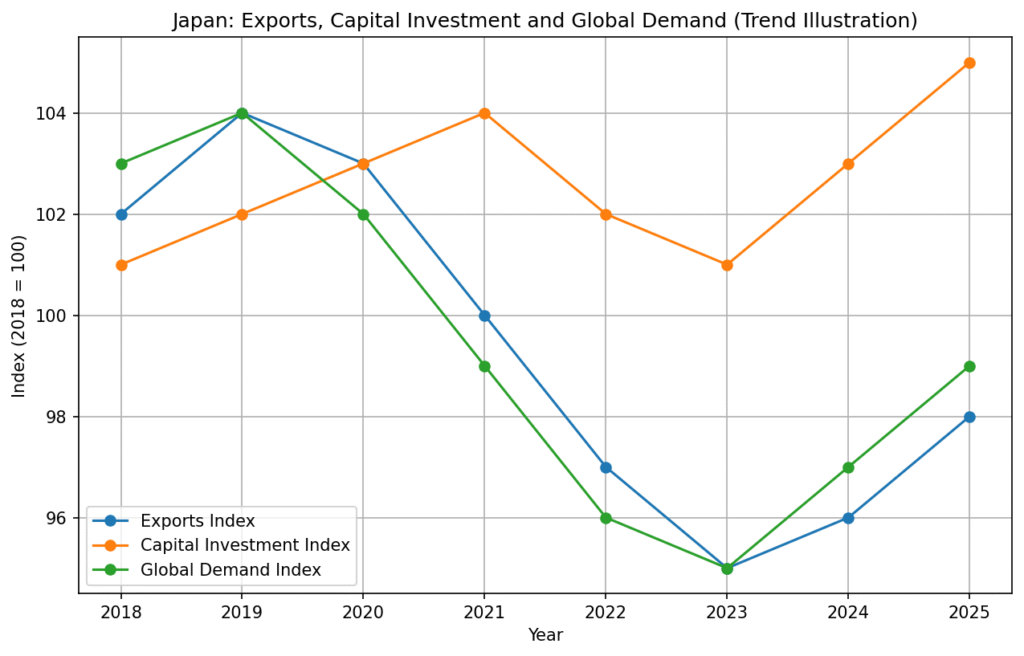

In the earlier phase of the forecast horizon, economic activity is expected to be supported by private consumption, exports and capital expenditure, aided by improving household income and steady global growth conditions. However, the report makes clear that this support will gradually weaken over time.

Demographics and Rates to Weigh Later

In the latter half of the projection period, structural headwinds are expected to become more visible. Accelerating population decline and rising long-term interest rates are both projected to act as drags on economic expansion.

Even so, consumption growth driven by wage increases is expected to provide a partial cushion, suggesting that domestic demand will remain an important stabilising force for Japan’s economy.

Inflation Expected Around Target

On the price side, the institute forecasts CPI inflation to average about 2.1% annually over the medium term, broadly consistent with the Bank of Japan’s price stability objective.

The interest-rate outlook reflects this environment. DIR expects the Bank of Japan to gradually raise short-term policy rates to around 1.75% by FY2027, signalling continued but measured monetary normalisation.

Long-term interest rates are projected to climb above 4% toward the end of the forecast window, partly due to a loosening supply-demand balance in government bonds.

Currency dynamics are also expected to shift gradually. The report projects the yen to appreciate against the U.S. dollar, potentially reaching the ¥111 per dollar range in the latter half of the forecast period.

A stronger yen would have mixed implications, potentially easing import costs while creating additional pressure for exporters.

Currency dynamics are also expected to shift gradually. The report projects the yen to appreciate against the U.S. dollar, potentially reaching the ¥111 per dollar range in the latter half of the forecast period.

A stronger yen would have mixed implications, potentially easing import costs while creating additional pressure for exporters.

Beyond growth, the report raises concerns about Japan’s fiscal trajectory. The primary balance of national and local governments is projected to remain in deficit throughout the forecast horizon, roughly in the –2.5% to –1.7% of GDP range under the baseline scenario.

DIR warns that policy measures such as consumption tax cuts or increased defence spending could widen the deficit significantly beyond current expectations. Rising long-term interest rates are also expected to push up net interest payments.

As a result, the overall fiscal balance could deteriorate markedly, with the deficit projected to widen to around –6.0% of GDP by FY2035.

The outlook for public debt is similarly nuanced. The ratio of outstanding public debt to GDP is expected to continue declining into the early 2030s, but the trend is projected to reverse later as interest costs rise and the primary balance deficit expands.

DIR stresses that relying solely on the debt-to-GDP ratio as a fiscal anchor could prove risky, since the metric is highly sensitive to economic conditions and interest-rate movements.

Taken together, the DIR assessment paints a picture of an economy that remains fundamentally stable but structurally constrained. Japan is expected to maintain moderate growth supported by wages and external demand, yet demographic decline and fiscal pressures will increasingly shape the long-term landscape.

For policymakers and investors, the key message is that Japan’s economy is not entering a downturn — but neither is it poised for a high-growth breakout.

Bottom line: Japan is projected to grow at roughly 0.8% annually through 2035, with inflation near target and interest rates gradually rising. The outlook is stable but capped by demographics and mounting fiscal challenges.

Beyond growth, the report raises concerns about Japan’s fiscal trajectory. The primary balance of national and local governments is projected to remain in deficit throughout the forecast horizon, roughly in the –2.5% to –1.7% of GDP range under the baseline scenario.

DIR warns that policy measures such as consumption tax cuts or increased defence spending could widen the deficit significantly beyond current expectations. Rising long-term interest rates are also expected to push up net interest payments.

As a result, the overall fiscal balance could deteriorate markedly, with the deficit projected to widen to around –6.0% of GDP by FY2035.

The outlook for public debt is similarly nuanced. The ratio of outstanding public debt to GDP is expected to continue declining into the early 2030s, but the trend is projected to reverse later as interest costs rise and the primary balance deficit expands.

DIR stresses that relying solely on the debt-to-GDP ratio as a fiscal anchor could prove risky, since the metric is highly sensitive to economic conditions and interest-rate movements.

Taken together, the DIR assessment paints a picture of an economy that remains fundamentally stable but structurally constrained. Japan is expected to maintain moderate growth supported by wages and external demand, yet demographic decline and fiscal pressures will increasingly shape the long-term landscape.

For policymakers and investors, the key message is that Japan’s economy is not entering a downturn — but neither is it poised for a high-growth breakout.

Bottom line: Japan is projected to grow at roughly 0.8% annually through 2035, with inflation near target and interest rates gradually rising. The outlook is stable but capped by demographics and mounting fiscal challenges.