PUBLISHED January 22, 2026

According to the Bank of Canada’s Business Outlook Survey for the fourth quarter of 2025, Canadian businesses ended 2025 in a cautious mood as economic uncertainty continued to shape daily operations. Weak domestic demand and slowing global growth made long-term planning more difficult for many firms. Although confidence improved slightly compared with the middle of the year, it remains below historical norms. Companies report that customers are more price-sensitive and hesitant to commit to large purchases. This has lengthened sales cycles and increased pressure on profit margins. At the same time, financing conditions remain tight for smaller firms. Together, these factors have encouraged a more conservative business mindset. Stability has become a higher priority than rapid expansion.

Expectations for sales growth in the year ahead remain modest across most sectors. Few companies anticipate a strong rebound in demand in the near term. Export-oriented firms are particularly cautious due to ongoing trade tensions with the United States. Uncertainty around tariffs and regulations continues to complicate contract negotiations. Some businesses have started to redirect exports toward Europe and Asia. However, building new markets requires time and additional investment. As a result, revenue forecasts remain restrained. Most firms are preparing for gradual rather than rapid improvement.

Business plans for investment reflect a similarly careful approach. Spending is mainly directed toward maintaining existing equipment and improving efficiency. Large expansion projects remain rare in the current environment. On the labor side, most companies report that staffing levels are sufficient. Widespread labor shortages have largely faded. Hiring intentions for 2026 are conservative. Many firms expect to keep headcounts unchanged. Others are considering small reductions if demand weakens further.

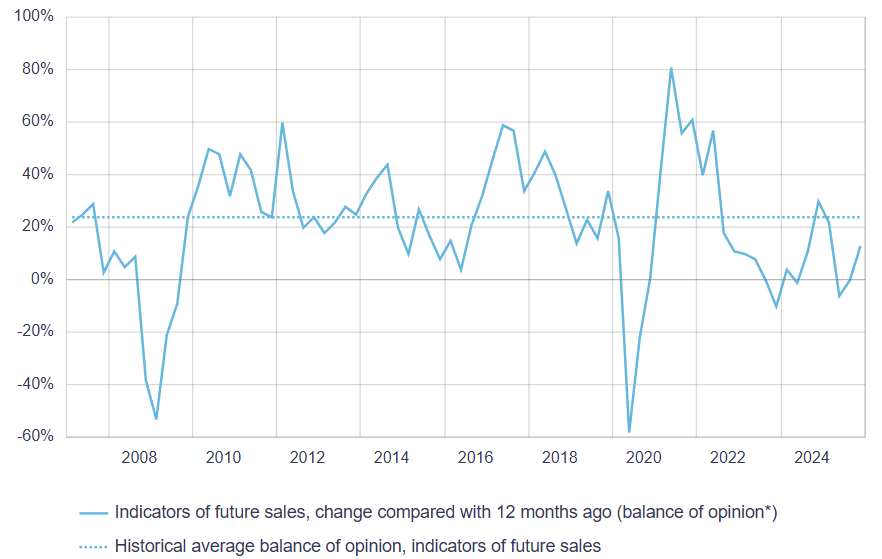

Sales performance over the past year has been disappointing for many Canadian firms. Approximately one-third of respondents reported declining volumes, while a large share saw little to no growth. Companies affected by trade disruptions experienced particularly weak results, as tariffs and regulatory barriers increased costs and reduced competitiveness. Looking forward, sales indicators show slight improvement. More firms now expect growth than contraction, but the anticipated pace remains slow. Businesses described future demand as “uncertain” and “highly dependent on external conditions,” including currency movements, geopolitical developments, and interest rate trends. Trade exposure plays a crucial role in shaping expectations. Firms heavily reliant on U.S. markets reported significantly lower confidence than those with more diversified customer bases. Some exporters have begun restructuring supply chains to reduce vulnerability, though this often involves higher short-term expenses. Ultimately, while the outlook for sales has improved marginally, it remains fragile and uneven across sectors.

Most Canadian businesses currently operate with sufficient production capacity. Weak demand means that factories, offices, and logistics networks are not under significant strain, reducing the need for major capital expansion. Investment plans reflect this reality. Although intentions have improved slightly, spending is primarily aimed at maintaining existing assets, improving cybersecurity, automating administrative tasks, and reducing energy costs. Large-scale projects remain rare, as firms hesitate to commit to long-term investments amid uncertain revenue prospects. The labor market tells a similar story. Shortages that dominated headlines in previous years have largely faded. Recruitment has slowed, wage pressures have eased, and employee turnover has declined. Many firms plan to freeze hiring in 2026, while a notable share is considering modest layoffs to align staffing levels with current workloads. This cautious approach highlights how closely employment decisions are tied to sales expectations. Overall, businesses are focused on efficiency, flexibility, and risk management rather than aggressive growth.

Source: Bank of Canada, Business Outlook Survey — Fourth Quarter of 2025 (BankofCanada.ca)

The chart shows that Canadian firms are becoming slightly more optimistic about future sales after a weak year. More companies now expect demand to improve than to decline, indicating that the worst phase of the slowdown may be over. However, the indicator is still below its long-term average, suggesting that businesses are not expecting strong growth. Instead, the data points to a slow and cautious recovery, shaped by ongoing trade uncertainty and subdued overall demand.

Sales performance over the past year has been disappointing for many Canadian firms. Approximately one-third of respondents reported declining volumes, while a large share saw little to no growth. Companies affected by trade disruptions experienced particularly weak results, as tariffs and regulatory barriers increased costs and reduced competitiveness. Looking forward, sales indicators show slight improvement. More firms now expect growth than contraction, but the anticipated pace remains slow. Businesses described future demand as “uncertain” and “highly dependent on external conditions,” including currency movements, geopolitical developments, and interest rate trends. Trade exposure plays a crucial role in shaping expectations. Firms heavily reliant on U.S. markets reported significantly lower confidence than those with more diversified customer bases. Some exporters have begun restructuring supply chains to reduce vulnerability, though this often involves higher short-term expenses. Ultimately, while the outlook for sales has improved marginally, it remains fragile and uneven across sectors.

Most Canadian businesses currently operate with sufficient production capacity. Weak demand means that factories, offices, and logistics networks are not under significant strain, reducing the need for major capital expansion. Investment plans reflect this reality. Although intentions have improved slightly, spending is primarily aimed at maintaining existing assets, improving cybersecurity, automating administrative tasks, and reducing energy costs. Large-scale projects remain rare, as firms hesitate to commit to long-term investments amid uncertain revenue prospects. The labor market tells a similar story. Shortages that dominated headlines in previous years have largely faded. Recruitment has slowed, wage pressures have eased, and employee turnover has declined. Many firms plan to freeze hiring in 2026, while a notable share is considering modest layoffs to align staffing levels with current workloads. This cautious approach highlights how closely employment decisions are tied to sales expectations. Overall, businesses are focused on efficiency, flexibility, and risk management rather than aggressive growth.

Source: Bank of Canada, Business Outlook Survey — Fourth Quarter of 2025 (BankofCanada.ca)

The chart shows that Canadian firms are becoming slightly more optimistic about future sales after a weak year. More companies now expect demand to improve than to decline, indicating that the worst phase of the slowdown may be over. However, the indicator is still below its long-term average, suggesting that businesses are not expecting strong growth. Instead, the data points to a slow and cautious recovery, shaped by ongoing trade uncertainty and subdued overall demand.

Reform PRODUCTS & SERVICES Group

Szentendrei út 87.

1033 Budapest

Hungary