PUBLISHED January 21, 2026

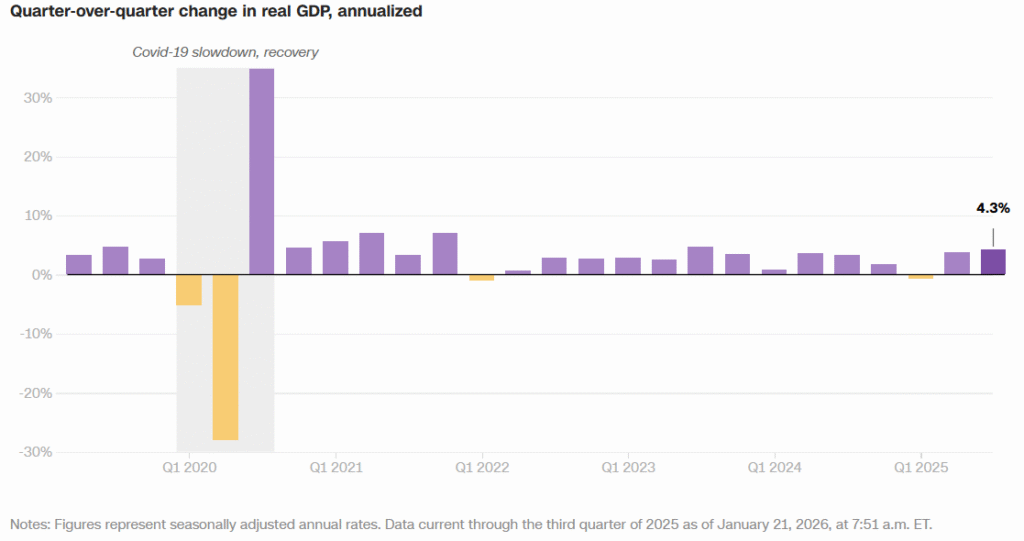

According to CNN Business, data from the U.S. Commerce Department showed that the United States economy grew at an inflation-adjusted annualized rate of 4.3% in the third quarter of 2025, significantly outpacing the previous quarter’s 3.8% pace. Consumer spending was a key driver, rising 3.5% from the second quarter, while exports surged by 8.8%, reversing earlier declines. Government expenditures, especially in defense and federal projects, also contributed positively to the expansion. This performance marks the fastest GDP growth in two years, even as the report reflected disparities across income groups and spending categories. The data release had been delayed by a government shutdown earlier in the fall, complicating comparisons with previous quarters. Some analysts warned that this unusual timing may temper the outlook for the final months of 2025. Despite these caveats, the headline figures underscored a resilient economy.

A deeper look at the GDP components reveals a complex mix of strengths and weaknesses in the U.S. economy. Export growth rebounded sharply, reversing earlier contractions, and bolstering overall output. Government consumption made a significant positive contribution, helping offset weaker private investment in structures and housing. However, investment in equipment and intellectual property products continued at a slower pace than earlier in the year, suggesting more cautious business spending. Imports declined further, which mechanically lifted the GDP figure but also pointed to softer domestic demand for foreign goods. This combination highlights that while certain sectors acquired momentum, others remain sluggish or volatile. Economists cautioned that the robust third-quarter reading may not fully withstand the slowdown expected in the fourth quarter as federal spending eases.

The initial GDP estimate for Q3 2025 surprised many economists with its 4.3% annualized growth rate, well above forecasted figures around 3.2–3.3%. Consumer expenditures increased significantly, supporting the broad economy’s expansion. Export performance rebounded strongly from earlier contraction, contributing to the headline figure. Government spending, particularly defense outlays, added further momentum. Despite slower investment in structures and housing, overall GDP climbed faster than at any time since Q3 2023. The turnaround from the prior quarter reflects resilience against earlier projections of slowing output. However, the underlying data quality may be clouded by the government shutdown that delayed several economic releases.

The initial GDP estimate for Q3 2025 surprised many economists with its 4.3% annualized growth rate, well above forecasted figures around 3.2–3.3%. Consumer expenditures increased significantly, supporting the broad economy’s expansion. Export performance rebounded strongly from earlier contraction, contributing to the headline figure. Government spending, particularly defense outlays, added further momentum. Despite slower investment in structures and housing, overall GDP climbed faster than at any time since Q3 2023. The turnaround from the prior quarter reflects resilience against earlier projections of slowing output. However, the underlying data quality may be clouded by the government shutdown that delayed several economic releases.

Consumer spending remains the primary engine of U.S. economic growth, with robust gains from higher-income households. Spending on goods and services such as travel, healthcare, and vehicles surged relative to earlier periods, reflecting strong balance sheets and accumulated savings among affluent consumers. Yet lower- and middle-income households exhibited more cautious outlays amid elevated living costs, higher borrowing rates, and persistent price pressures in essential categories such as housing and food. The disparity contributed to a K-shaped recovery pattern, with wealthier Americans capturing a disproportionate share of gains while others struggled to maintain purchasing power. Many consumers expressed concern about the jobs market and future financial security, particularly in sectors exposed to automation and global competition. Confidence indexes reflected this hesitancy, sliding to multi-year lows and signaling growing anxiety about income stability. Analysts warn that this uneven confidence could limit sustained consumption growth over the coming quarters. Lower consumer sentiment may weigh on retail and service sectors in the months ahead, especially if labor market conditions soften. If household caution deepens, the current pace of expansion could gradually lose momentum despite strong headline figures.

GDP composition reveals that not all sectors share equally in the recent expansion. Export volumes rebounded sharply from earlier contractions, improving net output contributions and benefiting manufacturing hubs and logistics providers. Government spending, boosted by defense programs and federal employment outlays, added notable strength to the economy and partially offset weakness in private investment. However, fixed investment, particularly in structures and residential construction, lagged behind other components as higher financing costs dampened new projects. Investment in equipment and intellectual property grew more slowly than earlier quarters, signaling cautious business sentiment amid geopolitical uncertainty and volatile demand forecasts. Import declines mechanically raised the headline GDP figure but also reflect reduced domestic demand for foreign goods and softer activity in consumer electronics and capital equipment. These mixed trends underscore how sectoral imbalances can shape macroeconomic readings in ways that mask underlying fragility. Economists caution that the momentum seen in Q3 may not be fully sustained into the final quarter of 2025 as fiscal stimulus fades and global growth moderates. A prolonged slowdown in investment could limit productivity gains and constrain long-term expansion if businesses delay modernization plans.

Source: CNN Business, U.S. Bureau of Economic Analysis (BEA), “U.S. GDP grows at fastest pace in two years in Q3 2025”, December 23, 2025

The chart shows that third-quarter GDP growth was overwhelmingly powered by consumer spending and government expenditure, while private investment made only a modest contribution. Exports also rebounded strongly, adding visible momentum compared with the previous quarter. At the same time, residential and business investment remain relatively weak, indicating that companies are still cautious despite strong headline growth. The visual balance of the components suggests that current expansion is demand-led rather than productivity- or capital-driven. This structure supports short-term growth but may limit longer-term economic sustainability if investment does not recover.

Consumer spending remains the primary engine of U.S. economic growth, with robust gains from higher-income households. Spending on goods and services such as travel, healthcare, and vehicles surged relative to earlier periods, reflecting strong balance sheets and accumulated savings among affluent consumers. Yet lower- and middle-income households exhibited more cautious outlays amid elevated living costs, higher borrowing rates, and persistent price pressures in essential categories such as housing and food. The disparity contributed to a K-shaped recovery pattern, with wealthier Americans capturing a disproportionate share of gains while others struggled to maintain purchasing power. Many consumers expressed concern about the jobs market and future financial security, particularly in sectors exposed to automation and global competition. Confidence indexes reflected this hesitancy, sliding to multi-year lows and signaling growing anxiety about income stability. Analysts warn that this uneven confidence could limit sustained consumption growth over the coming quarters. Lower consumer sentiment may weigh on retail and service sectors in the months ahead, especially if labor market conditions soften. If household caution deepens, the current pace of expansion could gradually lose momentum despite strong headline figures.

GDP composition reveals that not all sectors share equally in the recent expansion. Export volumes rebounded sharply from earlier contractions, improving net output contributions and benefiting manufacturing hubs and logistics providers. Government spending, boosted by defense programs and federal employment outlays, added notable strength to the economy and partially offset weakness in private investment. However, fixed investment, particularly in structures and residential construction, lagged behind other components as higher financing costs dampened new projects. Investment in equipment and intellectual property grew more slowly than earlier quarters, signaling cautious business sentiment amid geopolitical uncertainty and volatile demand forecasts. Import declines mechanically raised the headline GDP figure but also reflect reduced domestic demand for foreign goods and softer activity in consumer electronics and capital equipment. These mixed trends underscore how sectoral imbalances can shape macroeconomic readings in ways that mask underlying fragility. Economists caution that the momentum seen in Q3 may not be fully sustained into the final quarter of 2025 as fiscal stimulus fades and global growth moderates. A prolonged slowdown in investment could limit productivity gains and constrain long-term expansion if businesses delay modernization plans.

Source: CNN Business, U.S. Bureau of Economic Analysis (BEA), “U.S. GDP grows at fastest pace in two years in Q3 2025”, December 23, 2025

The chart shows that third-quarter GDP growth was overwhelmingly powered by consumer spending and government expenditure, while private investment made only a modest contribution. Exports also rebounded strongly, adding visible momentum compared with the previous quarter. At the same time, residential and business investment remain relatively weak, indicating that companies are still cautious despite strong headline growth. The visual balance of the components suggests that current expansion is demand-led rather than productivity- or capital-driven. This structure supports short-term growth but may limit longer-term economic sustainability if investment does not recover.