PUBLISHED January 22, 2026

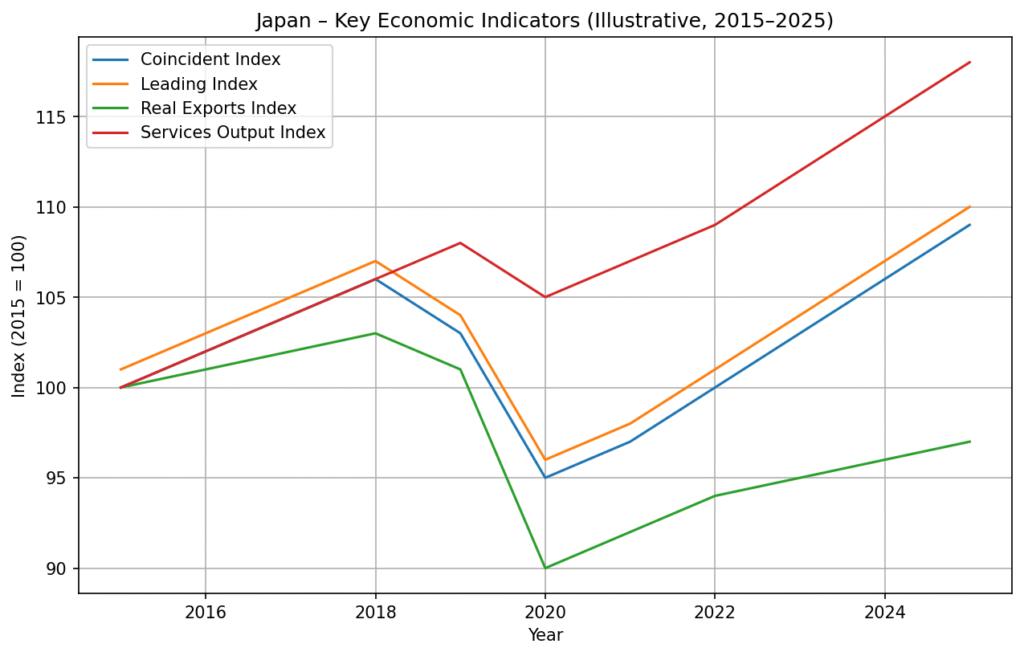

According to the Japan Research Institute’s December 2025 “Japan Economic Outlook” report, Japan’s overall economic conditions in late 2025 show a pattern of slow but steady improvement. Key indicators like coincident and leading indices have turned upward, reflecting that economic activity is recovering across several sectors. Household consumption continues to gain traction, supported by rising real incomes and improving consumer confidence. Service industries, including leisure and financial services, are expanding and contributing to growth momentum. However, manufacturing output and export performance remain softer than expected, dragging on broader activity. Employment conditions are favorable, helping sustain domestic demand. Inflation has shown signs of easing as energy and commodity price pressures relax.

Corporate profits have been rising, helped by lower energy costs and yen depreciation enhancing overseas revenue. Despite profit growth, investment in equipment and construction has temporarily slowed, with firms focusing on efficiency. Some companies are postponing large capital expenditures due to ongoing geopolitical uncertainty. Long-term investment in digital transformation and automation remains intact, albeit moderate. Export weakness, particularly to the U.S., has impacted business confidence and output in export-oriented sectors. At the same time, strong domestic demand has helped offset external headwinds for many firms. Business sentiment reflects cautious optimism.

Inflation trends point to a deceleration, with core price growth slowing toward the Bank of Japan’s target range. Lower energy and food cost pressures are primary contributors to the softening price environment. Nominal wages have been rising overall, helping support household spending and confidence. Consumer sentiment indicators have strengthened alongside stock market gains, adding to optimism. The central bank has maintained its policy stance but may consider tightening if wage growth persists. Global risks—including weak demand from China and trade tensions—continue to influence policy decisions. Overall, price and wage dynamics suggest measured progress toward sustained recovery.

Japan’s economic indicators show mixed but improving signals. Coincident indices, which track real-time economic activity, have rebounded, while leading indices suggest further moderate growth ahead. Household consumption has been resilient, buoyed by favorable labor conditions and rising real incomes. Services, especially in financial and information sectors, demonstrate stronger activity than manufacturing. Domestic firms report demand improvements, though exports remain a weak spot. Industrial production has been uneven, with some rebounds offset by sluggish factory output. Together, these trends point to a gradual recovery rather than a robust expansion.

Japan’s economic indicators show mixed but improving signals. Coincident indices, which track real-time economic activity, have rebounded, while leading indices suggest further moderate growth ahead. Household consumption has been resilient, buoyed by favorable labor conditions and rising real incomes. Services, especially in financial and information sectors, demonstrate stronger activity than manufacturing. Domestic firms report demand improvements, though exports remain a weak spot. Industrial production has been uneven, with some rebounds offset by sluggish factory output. Together, these trends point to a gradual recovery rather than a robust expansion.

Corporate earnings have reflected persistent resilience, supported by cost savings and currency effects. Profit margins improved as firms benefitted from lower import costs due to weaker energy prices. However, investment in physical capital has eased after several quarters of growth. Companies cite global trade uncertainty and cautious demand forecasts as reasons to defer large projects. Investment in digital and automation technologies continues to attract attention, but progress is measured. Export-oriented sectors face stiffer headwinds, dampening overall business sentiment. Domestic demand remains the primary driver of corporate performance.

Inflation in Japan has continued to ease toward the Bank of Japan’s target, as energy and imported commodity prices declined. Core consumer price growth has slowed, reducing cost pressure on households and businesses. At the same time, food price increases have stabilized, improving overall purchasing power. Service prices remain on a gradual upward path, mainly due to higher labor costs and steady domestic demand. This suggests that internal economic factors are now playing a larger role in shaping inflation than external shocks. Wages are rising moderately, supported by labor shortages in parts of the service sector and government pressure on firms to increase pay. As inflation cools, real wages are beginning to recover, helping to strengthen consumer confidence and spending. The central bank has kept its monetary policy unchanged but signaled that sustained wage growth could eventually justify a cautious policy shift. For now, global uncertainty and weak export demand argue for a careful and gradual approach.

Japan’s economic landscape at the end of 2025 reflects measured progress: consumption and employment trends support moderate expansion, while exports and capital investment flag areas of concern. Price growth is easing, and real incomes are rising, yet global risks—including soft external demand and geopolitical uncertainty—remain influential. Companies and policymakers are navigating a balance between sustaining domestic momentum and responding to international headwinds. Looking into 2026, growth is expected to continue slowly, with domestic activity likely to be the main source of economic resilience.

Corporate earnings have reflected persistent resilience, supported by cost savings and currency effects. Profit margins improved as firms benefitted from lower import costs due to weaker energy prices. However, investment in physical capital has eased after several quarters of growth. Companies cite global trade uncertainty and cautious demand forecasts as reasons to defer large projects. Investment in digital and automation technologies continues to attract attention, but progress is measured. Export-oriented sectors face stiffer headwinds, dampening overall business sentiment. Domestic demand remains the primary driver of corporate performance.

Inflation in Japan has continued to ease toward the Bank of Japan’s target, as energy and imported commodity prices declined. Core consumer price growth has slowed, reducing cost pressure on households and businesses. At the same time, food price increases have stabilized, improving overall purchasing power. Service prices remain on a gradual upward path, mainly due to higher labor costs and steady domestic demand. This suggests that internal economic factors are now playing a larger role in shaping inflation than external shocks. Wages are rising moderately, supported by labor shortages in parts of the service sector and government pressure on firms to increase pay. As inflation cools, real wages are beginning to recover, helping to strengthen consumer confidence and spending. The central bank has kept its monetary policy unchanged but signaled that sustained wage growth could eventually justify a cautious policy shift. For now, global uncertainty and weak export demand argue for a careful and gradual approach.

Japan’s economic landscape at the end of 2025 reflects measured progress: consumption and employment trends support moderate expansion, while exports and capital investment flag areas of concern. Price growth is easing, and real incomes are rising, yet global risks—including soft external demand and geopolitical uncertainty—remain influential. Companies and policymakers are navigating a balance between sustaining domestic momentum and responding to international headwinds. Looking into 2026, growth is expected to continue slowly, with domestic activity likely to be the main source of economic resilience.